Early Retirement

| | | | | | |

| Were We Lucky in Our Market Timing? |

We've heard it suggested that investment timing was crucial to our success in

retiring early -- that we started investing in the 1990’s when the stock market

was roaring and that the results we attained aren't necessarily repeatable by

others under today’s market conditions.

Is this true? Did we benefit from exceptional market timing?

In a word, no. Here's why:

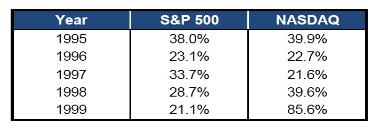

The “Roaring 90’s” were without question an amazing decade for investing.

Just take a look at these annualized returns from 1995 to 1999 to get an idea:

retiring early -- that we started investing in the 1990’s when the stock market

was roaring and that the results we attained aren't necessarily repeatable by

others under today’s market conditions.

Is this true? Did we benefit from exceptional market timing?

In a word, no. Here's why:

The “Roaring 90’s” were without question an amazing decade for investing.

Just take a look at these annualized returns from 1995 to 1999 to get an idea:

No one could complain about these investment returns! And if we had finished

our investing in the 90's then we would certainly agree our timing was

exceptional. However, since we started our investing in the 90’s the reverse is

almost true. After all, the whole point of investing is to buy low and sell high.

But we were buying high – then higher and higher. That was exactly what we

didn't want to be doing.

We saw our market timing as more of a hindrance than a help. We would have

preferred to have invested a decade earlier when markets were undervalued.

That way we would already have owned plenty of shares at reasonable

valuations by the time the 90’s came rolling around.

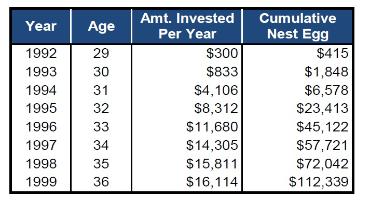

As novice investors we had very little money riding on the markets during

those years of extraordinary double-digit gains. The chart below shows our

annual investment amounts and cumulative nest egg from 1992 to 1999.

our investing in the 90's then we would certainly agree our timing was

exceptional. However, since we started our investing in the 90’s the reverse is

almost true. After all, the whole point of investing is to buy low and sell high.

But we were buying high – then higher and higher. That was exactly what we

didn't want to be doing.

We saw our market timing as more of a hindrance than a help. We would have

preferred to have invested a decade earlier when markets were undervalued.

That way we would already have owned plenty of shares at reasonable

valuations by the time the 90’s came rolling around.

As novice investors we had very little money riding on the markets during

those years of extraordinary double-digit gains. The chart below shows our

annual investment amounts and cumulative nest egg from 1992 to 1999.

As the chart shows, we were only able to invest very small amounts at first.

Even by 1997 our grand total was less than $58,000, so the big gains being

made in the stock market didn't help us all that much.

Keep in mind a 20% return on a $50,000 nest egg is $10,000, but a 20% return

on a $500,000 nest egg is $100,000. Thus having big market returns towards

the end of your investment window when your nest egg is bigger is much more

important than having them towards the beginning. By the end of the Roaring

90’s, after 8 years of investing, we had barely broken the $100,000 mark.

Over the 15-year period from 1992 to 2006 (when we retired), the S&P 500

returned 10.66% based on compound annual growth rates. But from 1997

(when we finally had $50,000 or more working for us) to 2006 the annual return

was only 8.41%. The long-term historical average is 9.15%, so our annualized

returns were solid but far from exceptional.

And once you factor in that we retired right into the Great Recession in 2007,

our timing suddenly doesn't seem quite so ideal, does it?

But our point isn't to suggest that our timing was bad but rather that ANY time is

a good time to invest if you maintain a long perspective. Even with stocks

soaring in the 1990’s, it was still a good time to invest because over the long

run stocks nearly always trend upwards.

It’s tempting to think others had it easier, or that market conditions were better

in some earlier time, but our recommendation would be to forget about all that

and just get out there and invest.

Even by 1997 our grand total was less than $58,000, so the big gains being

made in the stock market didn't help us all that much.

Keep in mind a 20% return on a $50,000 nest egg is $10,000, but a 20% return

on a $500,000 nest egg is $100,000. Thus having big market returns towards

the end of your investment window when your nest egg is bigger is much more

important than having them towards the beginning. By the end of the Roaring

90’s, after 8 years of investing, we had barely broken the $100,000 mark.

Over the 15-year period from 1992 to 2006 (when we retired), the S&P 500

returned 10.66% based on compound annual growth rates. But from 1997

(when we finally had $50,000 or more working for us) to 2006 the annual return

was only 8.41%. The long-term historical average is 9.15%, so our annualized

returns were solid but far from exceptional.

And once you factor in that we retired right into the Great Recession in 2007,

our timing suddenly doesn't seem quite so ideal, does it?

But our point isn't to suggest that our timing was bad but rather that ANY time is

a good time to invest if you maintain a long perspective. Even with stocks

soaring in the 1990’s, it was still a good time to invest because over the long

run stocks nearly always trend upwards.

It’s tempting to think others had it easier, or that market conditions were better

in some earlier time, but our recommendation would be to forget about all that

and just get out there and invest.